Derivatives have been far and away the fastest-growing sector within the cryptocurrency industry. An obvious extension of speculating via spot exchanges, derivatives now facilitate billions of dollars in value transfer every day, and as more external and institutional capital continues to flow into the space, cryptocurrency derivatives stand to play an ever increasing role in the markets.

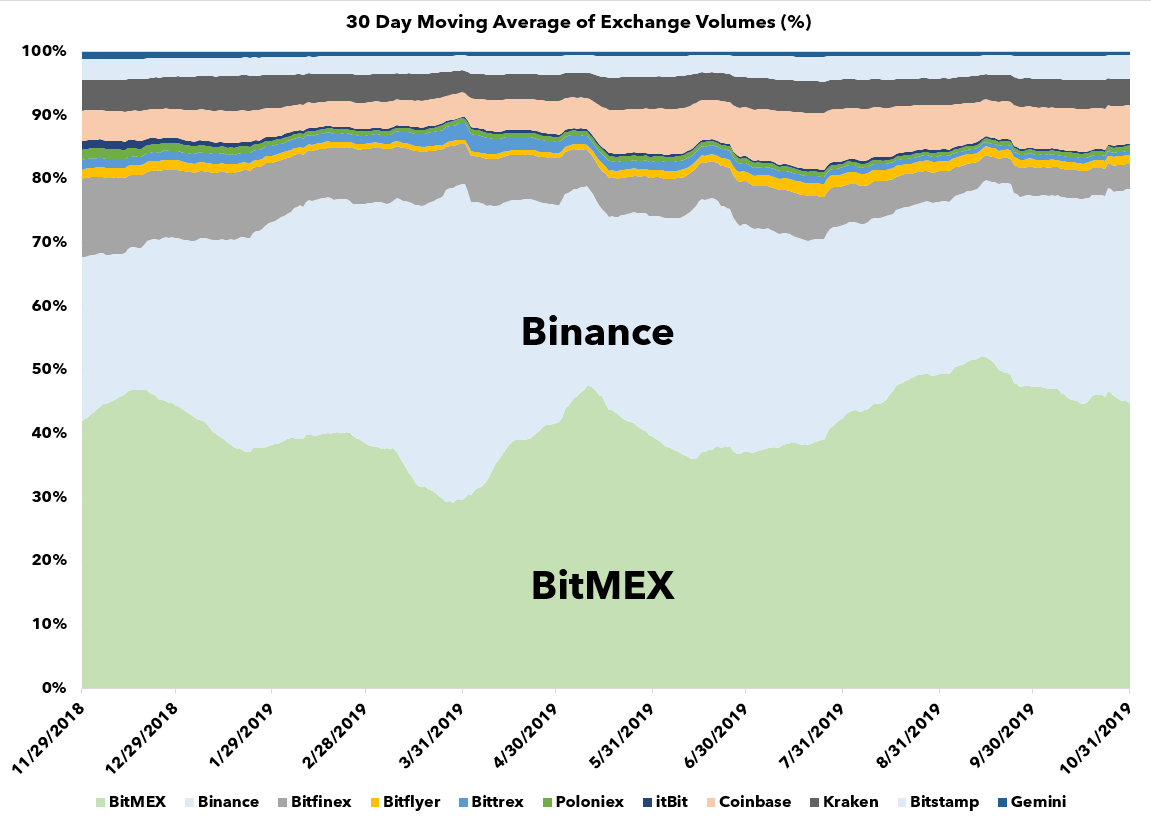

2019 has been a record year for cryptocurrency derivatives. For the first time, derivative volumes significantly outpace spot volumes on an an. Daily volumes on the leading derivatives exchanges now reach well into the 10’s of billions and the most popular derivatives exchanges like BitMEX regularly facilitate more than 200% the total volume across the top 10 most liquid spot exchanges.

Derivative markets being the dominant share of total trading volume means they’re increasingly becoming the main venue for price discovery. More recently, large movements in asset prices, especially Bitcoin, have been driven by margin liquidations. For example, the steep drop in price from ~$10,000 USD to ~$8,200 USD on September 24th, 2019 was exacerbated by over $700 million USD in margin liquidations on BitMEX. And while BitMEX historically has had an outsized effect on the crypto markets, new derivatives exchanges are coming to market rapidly, all of which offer a variety of financial products.

The rise of crypto derivatives has large implications for the overall crypto-asset market and by the looks of today’s growth, their influence will only grow stronger as the market continues to mature.

This post aims to provide a detailed overview of why cryptocurrency derivatives are seeing such immense growth, why they are important for the maturation of the crypto asset class, the different types of crypto derivative instruments, and the biggest players in the ecosystem today. At the end, we’ll briefly touch on what the future might hold for the cryptocurrency derivatives landscape.

Why it’s happening?

There are a number of factors that explain the emphatic rise of cryptocurrency derivatives.

First, cryptocurrency derivatives give investors more powerful ways to speculate on the future of value of cryptocurrencies. As the dominant crypto use case is still speculation, it logically follows that the largest entities in crypto will be the ones that allow individuals to speculate. Derivatives exchanges give investors access to a great amount of leverage, which allows them to take much larger bets than they would be able to otherwise, and far more than the margin allotted by spot exchanges. Think on the magnitude of 100x leveraged exposure.

Similarly, derivatives give investors the flexibility to create financial exposure while at the same time reducing counterparty risk. A trader who takes on a position with 5x leverage means that he can leave 5x the amount of assets off the exchange, making it much harder for an attacker to steal those coins relative to traditional centralized exchanges.

Second, derivatives give every cryptocurrency holder a medium to hedge the value of their assets. With derivatives, holders can offset downside to speculators who are willing to take the other side. This makes the underlying much more useful as holders can actually lock in the value of their assets. For example, miners can more effectively manage their CapEx by selling BTC through futures, buying put options, and selling call options.

The ability to hedge is what makes a fixed supply asset much more viable in the real world. Businesses and users are inherently short transaction fees, while miners, and the supply side more broadly, are long transaction fees. The supply side needs options and futures to lock in pricing for their services otherwise they’re constantly exposed to market volatility.

Third, accessing cryptocurrency derivatives markets is extremely easy. There are no account minimums, positions can be margined in crypto (they don’t have to touch any part of the existing financial system), liquidations are automatic, and all it takes to create an account is an email and password. Similarly, the fact that anyone in the world can access these markets makes it significantly easier to bootstrap liquidity at global scale. This last factor isn’t necessarily a net positive as the reason they’re able to enjoy relaxed restrictions is that they’re not heavily regulated. Some argue cryptocurrencies thrive in regulatory arbitrage scenarios and others would say regulatory scrutiny is coming. Only time will tell.

Why Derivatives are Important?

Derivatives are extremely powerful financial tools. Similar to traditional markets, cryptocurrency derivatives allow investors to get exposure to a contract whose value is derived from a specific cryptocurrency without ever touching the underlying currency itself.

More specifically, derivatives are a natural by-product of the continued institutionalization of the cryptocurrency market. Derivatives make it much easier for institutions to get exposure for a number of reasons:

Custody

- Many institutional investors aren’t interested in self custodying their own assets given both the operational risks of doing so as well as the complex regulatory requirements that mandate firms with certain AUMs outsource custody. Derivatives give institutions the ability to get exposure to cryptocurrencies without the complexities of actually managing their own private keys. For example, CME provides BTC exposure to firms that otherwise would never want to go through the burden of setting up their own Bitcoin wallet or finding a qualified custodian.

Supply Constraints

- While Bitcoin’s 21 million supply cap is one of its most widely regarded tenets, this deflationary effect also makes it difficult for buyers to get exposure in really high volumes (inherent to the design). With derivatives, institutions purchase contracts rather than the underlying, so in theory, there could be more than 21 million BTC worth of notional exposure.

Risk Management

- Lastly, and most importantly, institutions rely on derivatives as an integral tool for managing risk. With spot exchanges alone, the view that market participants convey is limited given you can only really buy or sell. With derivatives, you can express your market view with granular precision and construct custom exposure. For example, if you want to hedge against BTC downside without having to sell your BTC, you can actually go short on a number of derivatives exchanges and create a synthetic USD position. This also has tax benefits as investors can lock in a dollar value without actually having to sell into dollars and incur a tax hit.

For all of the jokes regarding institutional participation in the space, the growth of derivatives is very much evident that they have indeed entered the cryptocurrency markets. Are they the same “institutions” that play in traditional asset classes? Probably a bit different, but most important is that more capital can now enter the space and a burgeoning derivatives market will only increase this trend.

Types of Derivatives

The fact that with a derivative you can create more granular risk exposure, means there’s really an unbounded design space for building financial products. Derivatives can turn most beliefs into a financial position. That’s why there’s no surprise cryptocurrency derivatives have grown so quickly given that the market today is essentially a set of competing belief systems. And just like in traditional forex markets, it’s important for market participants to express views against all currencies, not just a base one.

To date, the three most popular derivative products have been perpetual swaps, futures, and options.

Perpetual Swap

The perpetual swap is an instrument popularized by BitMEX, which allows users to get derivative exposure to Bitcoin without an expiration date. Unlike futures which have an expiry date, perpetual swaps settle periodically against some index price. Swaps have this feature because market participants pay some amount of funding based on the instrument’s price relative to the index price. If the funding rate, which is comprised of an interest rate component and a premium/discount component, is positive, longs pay shorts, and if it’s negative, shorts pay longs.

Perpetual swaps are by far the most popular product within the cryptocurrency derivatives market because they are the most liquid way for traders to essentially make BTC with their existing BTC. With the swap, you don’t need additional fiat to get exposure to Bitcoin’s price movements. BitMEX’s perpetual swap now does well over $1.5 billion USD in notional volume daily, getting up to even $12b as recently as Oct 26th 2019. Similarly, the fact that traders can access perpetual futures without providing any KYC information has likely been a driver of growth.

It’s also important to highlight the fact that perpetual swaps don’t exist in traditional markets, which is primarily a function of settlement and recourse risk. The mechanics that make crypto-native derivatives exchanges unique from their traditional counterparts was outlined well in this piece from Deribit Insights.

Futures

Futures allow investors to buy contracts that obligate them to buy or sell a cryptocurrency at a specific price. Futures can be either physically settled or cash settled, with most of today’s popular derivative exchanges are all cash-settled, but with the “cash” paid out in BTC. As an aside, this confuses many people who wish to begin trading. The futures are usually not physically settled -- but rather cash-settled, with the cash being paid out in bitcoin.

Futures are particularly useful tools for holders who want to lock in a specific price, for example, miners or hedgers. They also present a wide array or arbitrageurs who are willing to take on risk. For example, the infamous cash and carry Bitcoin futures trade.

Options

Options are just now coming to market, but they are already seeing very strong growth. Options grant investors and speculators the right to buy or sell a cryptocurrency at a specific price (but not the obligation).

In the futures world, each contract is worth $1 USD. This is not true in the options world. The value of options contracts fluctuates relative to a number of factors, mathematically expressed via the black-scholes equation.

Options are the most nimble derivatives product in the cryptocurrency market so far as they allow investors to speculate both price and volatility in a simple format. This is extremely powerful because volatility could have statistical relationships with other assets, and therefore new financial exposure can be created to manage certain risks.

Looking Ahead

While the products offered in the cryptocurrency derivatives market have been similar to those offered in traditional markets, cryptocurrency derivatives platforms have actually been quite innovative on the traditional exchange business model. Piggy backing off of Binance’s success with BNB, many of today’s largest derivatives exchanges have created tokens not only as a medium for their own value capture, but also as a medium for the end customer to receive some equity, dividend and/or fee discounts. This actually isn’t too far off from what traditional derivatives exchanges have offered previously via membership seats.

While regulatory clarity around exchange tokens is dubious, these assets may very well be the first glimpse into a world where many cryptocurrencies are backed with actual cash flows. These exchange tokens (while not technically equity) look and behave similarly to equity, with price movements largely reflecting the respective exchange’s performance. It also seems like the market is agreeing with this thesis as most investment has crowded into two buckets: 1) top market cap coins and 2) exchange tokens. As the reach and impact of exchanges continues to expand, native exchange tokens might be the best way to get exposure to this growth.

A few of the primary components that drive user demand for these tokens are fee discounts and buy/burn mechanisms that attempt to mimic a share buyback. The discounts are obviously priced in a way that it makes financial sense for large volume traders to buy and hold them. On the share buybacks, the premise is pretty simple. Exchanges take a portion of their top line revenue and use that money (BTC, USD,or a stablecoin) to buy their own token on the open market. Once the tokens are bought, they are taken out of supply, essentially decreasing the total number of future coins the exchange could then buy. Something interesting to point out is that the economics of these tokens is centralized which means exchanges can (and have been!) increasing the benefits to lure customers. The high degree of competition in the industry should end up benefiting users the most.

With so much saturation in the market, exchanges will have to start differentiating themselves by introducing novel products. Low hanging fruit seems like expansion of FTX’s indexes and leveraged tokens and their additional volatility products. Hash rate futures have long been folklore in the cryptocurrency industry, but nothing has materialized to date. There’s a chance that with the new liquidity and attention captured by derivatives today, hash rate markets, transaction fee markets, and much, much more could soon be created.

Another interesting development is the creation of smart contract based cryptocurrency derivatives. Regardless of how much more efficient derivatives make the crypto markets, many of today's exchanges are playing in a legal grey area. There will likely come a time where regulators will look to install more roadblocks to accessing crypto derivatives, which means platforms that can operate through code alone will see increased usage. A number of "DeFi" projects are working to create non-custodial versions of BitMex's perpetual swap as well as cryptocurrency options. This topic will likely be the discussion of a separate post, but something like a BTC/DAI future might be the holy grail of native crypto banking.

In terms of open questions, the biggest uncertainties remain around regulation. Many exchanges currently operate in a legal gray area, and most exchanges now bar U.S customers. Prohibiting US customers has been commonplace in the cryptocurrency derivatives industry, which has opened up the opportunity for more regulated avenues to emerge. Regulated entities such as Bakkt, ErisX, LedgerX and the CME are now fighting for control, but none have the token draw of their unregulated counterparts.